★★★

Advanced

(Double click on a word in the text to open the dictionary)

In this opening section, we will take a look at how the futures market works, how it differs from other markets and how the use of leverage impacts your investing. How Futures Work

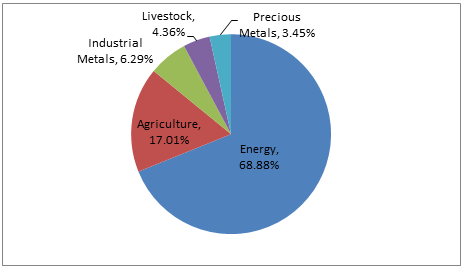

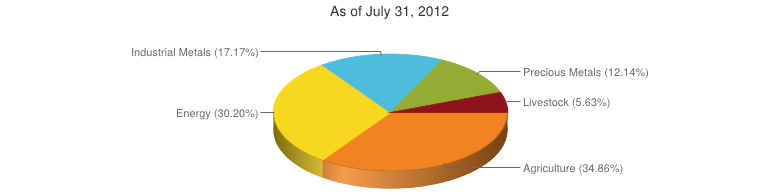

You are probably familiar with the concept of financial derivatives. A derivative is simply any financial instrument that “derives” its value from the price movement of another instrument. In other words, the price of the derivative is not a function of any inherent value, but rather of changes in the value of whatever instrument the derivative is tracking. For example, the value of a derivative linked to the S&P 500 is a function of price movements in the S&P 500. Futures are among the oldest derivatives contracts. They were originally designed to allow farmers to hedge against changes in the prices of their crops between planting and when they could be harvested and brought to market. As such, many futures contracts focus on things such as livestock (cattle) and grains (wheat). Since these beginnings, the futures market has expanded to include contracts linked to a wide variety of assets, including precious metals (gold), industrial metals (aluminum), energy (oil), bonds (Treasury bonds) and stocks (S&P 500). There are several different ways of measuring the commodities market, and the performance of different indexes can be vastly different. The charts below show the index composition of two popular commodity indexes. As you can see, the index sector weightings are quite different, with the result that performance can vary greatly. Therefore, it can be difficult to get a single view as to how the overall “commodity market” is performing. Goldman Sachs Commodity Index Sector Breakdown

Figure 1: Goldman Sachs Commodity Index Sector Breakdown

Dow Jones-UBS Commodity Index

Figure 2: Dow Jones-UBS Commodity Index

How Futures Differ from Other Financial Instruments

Futures differ in several ways from many other financial instruments. For starters, the value of a futures contract is determined by the movement of something else – the futures contract itself has no inherent value. Secondly, futures have a finite life. Unlike stocks, which can stay in existence forever, a futures contract has a set expiration date, after which the contract ceases to exist. This means that when trading futures, market direction and timing are vitally important. You will usually have some choices when choosing how long you want to make a wager for. For instance, there might be futures contracts on soybeans with expiration dates spaced every couple months for the next year and a half (i.e., December 2012, March 2013, June 2013, August 2013, December 2013.) While it might be obvious that the longest contract gives you the most time for your opinion to be right, this extra time comes at a cost. Longer-dated futures contracts will usually (but for reasons beyond the scope of this article, not always) be more expensive then shorter-dated contracts. Longer-dated contracts can sometimes be illiquid as well, further increasing your cost to buy and sell. A third difference is that in addition to making outright wagers on the direction of the market, many futures traders employ more sophisticated trades the outcomes of which depend upon the relationship of different contracts with each other (these will be explained later in this guide). Perhaps the most important difference, however, between futures and most other financial instruments available to individual investors involves the use of leverage. SEE: Futures Fundamentals: Introduction

Leverage

When buying or selling a futures contract, an investor need not pay for the entire contract at the time the trade is initiated. Instead, the individual makes a small up-front payment in order to initiate a position. As an example, let’s look at a hypothetical trade in a futures contract on the S&P 500. The value of this contract, which trades on the CME, is $250 times the level of the S&P 500. So, at a recent level for the S&P of approximately 1400, the value of the futures contract is $350,000 ($250 X 1400.) In order to initiate a trade, however, an individual only needs to post an initial margin of $21,875 (per current CME exchange margin requirements found on CME Group’s equity index products chart). Note: initial and maintenance margin levels are set by the exchanges and are subject to change.

So what happens if the level of the S&P 500 changes? Well, if the S&P rallies to 1500, which is slightly more than a 7% increase, the contract would be worth $375,000 ($250 X 1500.) Remember, that our investor only posted an initial margin of $21,875, but has now achieved a $25,000 profit for a-better-than 100% gain. This ability to achieve such a large profit even given a relatively modest move in the underlying index is a direct result of leverage and is one of the reasons that some people like to trade futures. Let’s now look, however, at what might happen if the S&P 500 fell in value. If the S&P fell ten points to 1390, the contract would be worth $347,500, and our investor would have a loss of $2500. Each day, the exchange will compare the value of the futures contract to the client’s account and either add profits or subtract losses to the client’s initial margin balance. The exchange requires that this balance stay above certain minimum levels, which in the case of the S&P 500 is $17,500. So in our example the trader would have a paper loss of $2500, but would not be required to post any additional cash to his or her account. What would happen if the S&P fell to 1300? In that case, the futures contract would only be worth $325,000 and the client’s initial margin of $21,875 would be wiped out. (Remember, leverage works both ways, so in this case a slightly more than 7% fall in the S&P would result in a complete loss of an investor’s money.) If this occurred, the individual would be hit with a margin call, and would be required to deposit more funds into his or her account in order to bring the balance back up. Read more: Beginner’s Guide To Trading Futures: The Basic Structure of the Futures Market |

Investopedia http://www.investopedia.com/university/beginners-guide-to-trading-futures/basic-structure-futures-market.asp#ixzz43uFph000

Comments are closed.